By Michael J. Devereux II, CPA, CMP

This summer, the American Mold Builders Association (AMBA) conducted its second micro-survey regarding the R&D tax credit. The first survey, conducted in 2015, had participation from 39 mold builders, 18 of which were claiming the credit at the time. This year, more than 60 molds shops were surveyed, 28 of which report claiming the R&D tax credit. Of those 28 companies, 60% also are claiming state R&D tax credit.

As Chart 1 represents (and the above data indicates), the R&D tax credit – short for the US Credit for Increasing Research Activities – is one of the most underutilized tax savings opportunities for companies in the mold manufacturing industry, regardless of company sales. Because this tax credit rewards companies that invest resources in innovation, product development, mold design, new materials or resins and process development/improvement, mold builders have many potential opportunities to claim this credit and reduce their federal and state tax liabilities.

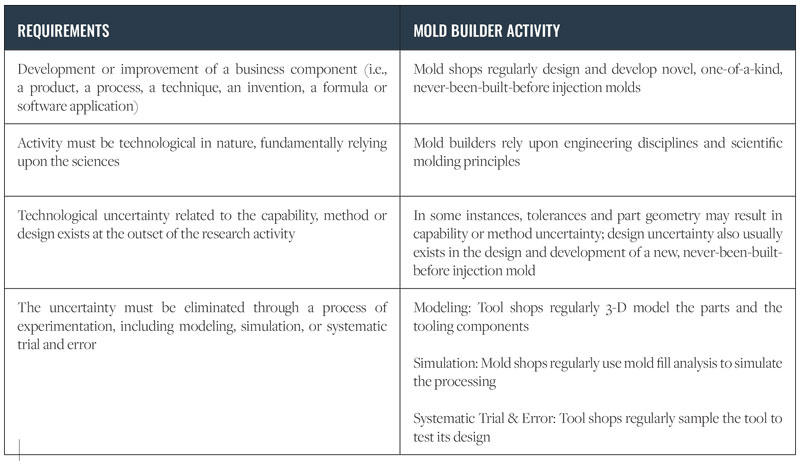

General Requirements for Qualifying Activities

In order to claim the credit, the mold builder must engage in qualified research activities. There are four general requirements for an activity to qualify for the credit, which are listed in Chart 1.

As such, the types of activities that may qualify for the R&D tax credit may include, but are not limited to, the following:

- Developing new mold designs

- Developing tool-specific fixturing

- Sampling new tool designs

- Improving manufacturing processes through automation

- Experimenting with new alloys

- Performing PPAP or First Article inspections on new molds

Fact or Myth: Only Large Companies Benefit from the R&D Tax Credit

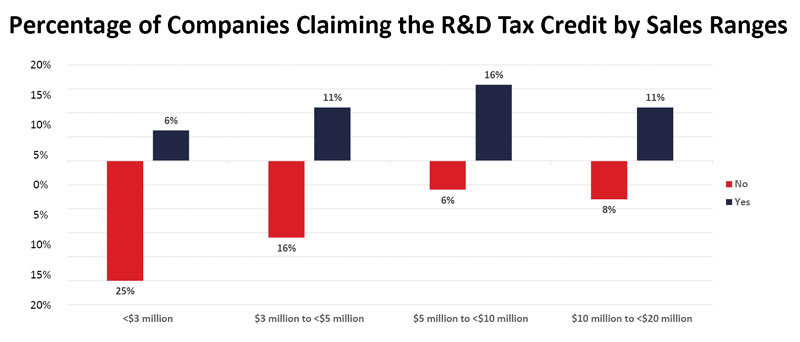

Despite what many believe, companies participating in such activities as those listed in Chart 1 are not only those larger in size. In fact, data gathered from this year’s survey indicated that, although companies that report under $3 million in sales (and/or zero to 10 employees) are the smallest percentage of respondents claiming the R&D tax credit, other revenue and employee ranges show quite a few companies taking advantage of this program. In fact, the most common range of respondent companies that report claiming this credit tend to be midsize companies, with between 26 and 50 employees and – on average – reporting between $5 million and $10 million in sales. See Chart 2.

Types of Qualifying Expenditures

Within these activities, there are three types of expenditures that qualify for the R&D tax credit: Wages paid for the performance of qualified services; supplies and materials that are used in the conduct of the mold shop’s research efforts; and contract research, in which tool shops pay third parties to perform research on their behalf or test/sample their mold designs.

Of those claiming the credit, approximately 60% of the respondents indicated that they have amended their tax returns to claim the R&D tax credit in tax years they had not claimed the credit. Only three of the respondents had been through an IRS examination related to the R&D tax credit. In each case, the respondent company had amended its returns to claim the credit in prior years. Amending returns to claim the credit does not, necessarily, result in an IRS examination. However, this data point is worth noting.

Seventy-eight percent of the mold builders claiming the R&D tax credit reported that they are claiming the cost of labor and materials used to construct novel, one-of-a-kind injection molds. Two factors must exist for these expenditures to qualify. First, the mold shop must be at risk for the development of the mold and meeting the specifications identified in the contract or purchase order. Second, the appropriate design of the injection mold must still be uncertain at the time the mold is produced, assembled and sampled. That is, the testing or sampling of the injection mold will help the mold builder determine whether the mold is the appropriate design or whether modifications are necessary to meet the specifications. Experimentation must occur with the injection mold. As one might suspect, those shops including these types of expenditures are reporting significantly greater R&D tax credits.

The R&D tax credit is one of the most significant ways that mold builders can reduce their overall income tax liabilities. Proper documentation is critical to claiming and substantiating the research tax credit. Mold shops should regularly review their cost capturing methodologies and the types of expenditures that are being included to ensure these shops are claiming the proper amount of tax credit.

This analysis was provided by Michael Devereux II, CMP of Mueller Prost, an AMBA Partner, to prove an analysis of the aggregated data. Devereux is one of the leading authorities on application of the R&D tax legislation and has been used by a vast number of AMBA members to correctly structure their credit applications. For more information, visit www.muellerprost.com.