By Dianna Brodine, managing editor

The American Mold Builder

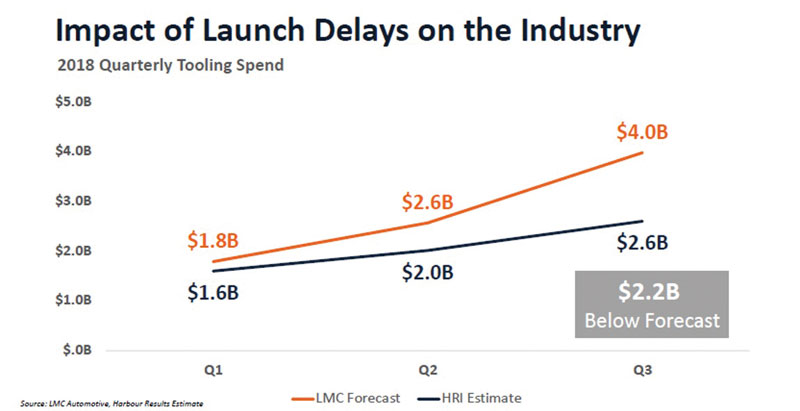

At the end of October, Harbour Results, Inc. (HRI) and OESA released the results of the annual study on the current state of the automotive vendor tooling industry, saying the industry is on track to miss the previously projected tooling spend for 2018 by $2.2 billion. Less than a month later, General Motors announced large-scale layoffs of more than 14,000 employees and the closure of five plants in North America. Ford also is expected to announce layoffs in early 2019 after its CEO suggested the tariffs enacted by the Trump administration could cost the company $1 billion, and Fiat-Chrysler already has enacted short-term layoffs at certain North American facilities.

North America isn’t the only area experiencing challenges in the automotive arena – China posted declines in auto sales for three straight months in the latter part of 2018, according to the China Association of Automobile Manufacturers (CAAM).

Bright spots remain, however. Despite failures by the automotive industry to maintain the gains of 2016 and 2017, HRI anticipates annual tooling spend will remain stable through 2021, offering encouragement for toolmakers with a high percentage of transportation-related customers.

Forecast data and commentary

2018 was supposed to be the big year for tooling. “The industry experienced a boom in 2017 with $10.3 billion in tooling spend and, based on the data, we expected 2018 to reach over $11 billion,” said Laurie Harbour, HRI president and CEO. “However, due to a number of vehicle cancelations and delays, we are predicting the year to be closer to $9.2 billion. The industry is $2.2 billion below forecast through the first three quarters of 2018, resulting in a six-point dip in tooling shop utilization to 79 percent.”

The key factor driving decreased tooling spend is the decreased number of North American vehicle launches predicted between 2019 and 2021 – 153 vehicles – versus the number of vehicles launched in North America between 2016-2018 – 183 vehicles. Furthermore, the Detroit 3 automakers, which source approximately 80% of their tools in this region, according to Harbour Results estimates, are forecasted to source only nine vehicles in 2019.

Factors in the slow down include a continued shift in consumer demand to SUVs and CUVs, away from sedans. In addition, the loan market for autos is tightening as banks such as Wells Fargo and Bank of America have reduced their auto lending portfolios by nearly 18% and more than 4.5%, respectively, according to quarterly earning disclosures reported by Forbes.

Still, the shifts affecting 2018’s projections could provide some stability for future years, as HRI anticipates that some of what was planned for 2018 will spill into 2019 to help level out the tooling spend for the next three years. The Detroit 3-dominated North American tooling market (approximately 80% of D3 tooling is produced in North America, according to Harbour estimates) is seeing a lot of quote activity, but it’s focused on design work, so the actual hours put into tooling production won’t happen until 2019.

In addition to the 2019 forecast of $8 billion in automotive vendor tooling, Harbour IQ estimates future North American tooling spend to remain relatively stable, with 2020 totaling $8.2 billion and 2021 at $9 billion.

Based on quote activity and the forecasts, toolmakers may feel confident. However, it’s yet to be determined how much impact new tariff restrictions will have on pricing for car parts, steel and resin, and fuel surcharges also will have an effect.

“This forecast is based on current data and information, but issues like tariffs, automaker restructuring and/or an economic recession could drastically impact the forecast, resulting in a dip in tooling spend as much as $2 billion,” said Harbour.

“As the tooling market contracts, it is important that shops, specifically small shops that benefited from the increased outsourcing in 2017, prepare for the future,” she continued. “It is important that tool shops continue to focus on improving operations, making smart investments in people and technology, and strategic planning to remain competitive in the near and long term.”